| Forecast Period | 2024-2032-2029 |

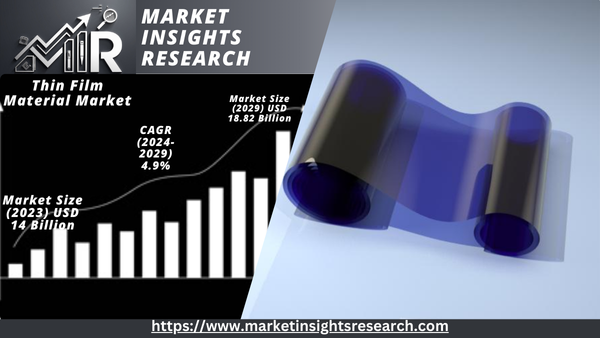

| Market Size (2023) | USD 14 Billion |

| Market Size (2029) | USD 18.82 Billion |

| CAGR (2024-2029) | 4.9% |

| Fastest Growing Segment | Optical Coating |

| Largest Market | Asia Pacific |

Market Overview

Global Thin Film Material Market was valued at USD 14 Billion in 2023 and is expected to reach at USD 18.82 Billion in 2030 and project robust growth in the forecast period with a CAGR of 4.9% through 2029.

Download Sample Ask for Discount Request Customization

The global thin film material market is experiencing substantial growth, driven by the expanding applications in electronics, renewable energy, and advanced manufacturing. Thin film materials, characterized by their lightweight and flexible nature, are crucial in the production of cutting-edge technologies such as semiconductors, photovoltaic cells, and displays. The market is bolstered by the rising adoption of thin film technologies in consumer electronics, including smartphones, tablets, and wearable devices, which demand high-performance and space-efficient components. Additionally, the push for renewable energy solutions, such as solar panels, further fuels market expansion, as thin film photovoltaic cells offer an economical and efficient alternative to traditional silicon-based panels. Technological advancements and innovations in deposition techniques, such as Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD), enhance the performance and application range of thin film materials, driving further growth. The increasing focus on sustainability and energy efficiency also contributes to the market's rise, with thin films providing essential benefits in reducing material usage and improving energy efficiency. As industries continue to innovate and seek advanced material solutions, the thin film material market is poised for continued expansion.

Key Market Drivers

Advancements in Electronics and Consumer Devices

The rapid advancements in electronics and consumer devices are a primary driver of the global thin film material market. As electronic devices become increasingly sophisticated, there is a growing need for components that are both lightweight and high-performance. Thin films, due to their unique properties, such as high electrical conductivity and flexibility, are essential in the manufacture of modern electronic components, including displays, sensors, and semiconductors. The trend towards miniaturization in electronics, driven by consumer demand for more compact and versatile gadgets, further accelerates the use of thin film materials. Innovations in areas such as flexible electronics and wearable technology rely heavily on thin films to provide essential functionalities in a compact form factor. As technology continues to evolve, the demand for advanced thin film materials that can meet the performance and durability requirements of next-generation electronics is expected to grow, driving market expansion.

Growth in Renewable Energy Sector

The growth of the renewable energy sector, particularly solar energy, significantly impacts the global thin film material market. Thin film photovoltaic cells, which use thin layers of semiconductor materials to convert sunlight into electricity, offer a cost-effective and efficient alternative to traditional silicon-based solar panels. These thin film technologies can be applied to a variety of surfaces and are less material-intensive, making them a favorable choice for large-scale solar installations as well as for integrating into building materials. The increasing focus on sustainable energy solutions and government incentives for renewable energy adoption further drive the demand for thin film materials. As solar energy becomes a more prominent component of the global energy mix, the need for innovative thin film materials that enhance the efficiency and affordability of solar panels will continue to rise, fueling market growth.

Download Sample Ask for Discount Request Customization

Technological Innovations in Deposition Techniques

Technological innovations in deposition techniques are a crucial driver for the thin film material market. Advances in deposition technologies, such as Chemical Vapor Deposition (CVD), Physical Vapor Deposition (PVD), and Atomic Layer Deposition (ALD), have significantly improved the quality and performance of thin films. These advanced techniques allow for the precise control of film thickness, composition, and uniformity, which are essential for achieving high-performance thin film applications. The continuous development of these technologies enables the production of thin films with enhanced properties, such as better conductivity, durability, and optical characteristics. As industries seek to leverage these innovations for various applications, including electronics, energy, and coatings, the demand for advanced thin film materials driven by cutting-edge deposition techniques is expected to grow, propelling market growth.

Increasing Demand for Flexible and Wearable Electronics

The rising demand for flexible and wearable electronics is a significant driver of the thin film material market. Flexible electronics, which incorporate thin film materials, offer the advantage of being lightweight and adaptable to various surfaces, making them ideal for applications such as flexible displays, electronic skin, and wearable devices. The proliferation of wearable technology, including fitness trackers, smartwatches, and health-monitoring devices, requires thin films that can provide essential functionalities while maintaining flexibility and durability. Additionally, advancements in materials science have led to the development of thin films with enhanced mechanical properties, enabling their use in innovative flexible and stretchable electronic applications. As consumer interest in wearable technology and flexible electronics continues to grow, the demand for thin film materials that support these applications will drive market expansion.

Key Market Challenges

High Production Costs

One of the significant challenges facing the global thin film material market is the high production costs associated with manufacturing advanced thin films. The cost of raw materials, coupled with the sophisticated technology and equipment required for deposition processes like Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD), can be substantial. Additionally, achieving the precise control over thickness and uniformity of thin films, necessary for high-performance applications, often involves expensive and complex machinery. These high production costs can make thin film materials less competitive compared to traditional materials, particularly in price-sensitive markets. The challenge is compounded by the need for continuous research and development to innovate and reduce costs while maintaining high performance. To mitigate this challenge, companies are investing in improving production efficiencies, exploring cost-effective raw materials, and developing scalable manufacturing techniques. However, until these advancements are widely adopted, the high costs remain a significant barrier to market growth and widespread adoption of thin film technologies.

Download Sample Ask for Discount Request Customization

Technological Complexity and Integration Issues

The technological complexity involved in the development and integration of thin film materials poses a challenge for the market. Thin film technologies require advanced manufacturing processes and precise control over deposition techniques to achieve desired properties and performance. Integrating these thin films into existing systems and devices can be complex, particularly when adapting to various applications such as electronics, solar panels, and coatings. The challenge lies in ensuring compatibility with existing technologies and achieving optimal performance across different applications. Moreover, advancements in thin film technologies are rapidly evolving, and staying abreast of the latest developments can be challenging for manufacturers and end-users alike. Addressing these complexities requires ongoing investment in R&D, as well as collaboration between technology providers and industry stakeholders to ensure seamless integration and performance. Failure to effectively manage these technological challenges can hinder the adoption and growth of thin film materials in various applications.

Limited Raw Material Availability

The availability of raw materials used in thin film production poses another challenge for the global market. Many thin films are produced using materials that are rare or have limited supply, such as indium, tellurium, and various rare earth elements. The reliance on these materials can lead to supply chain constraints and price volatility, impacting the stability and cost of thin film products. Additionally, the extraction and processing of these raw materials often involve environmental and geopolitical issues, further complicating their availability. To address this challenge, companies are exploring alternative materials and recycling technologies to reduce dependence on scarce resources. Efforts are also being made to develop more sustainable and cost-effective sources of raw materials. However, until these solutions are fully realized, the limited availability of key raw materials remains a significant challenge for the thin film material market, affecting both production costs and supply stability.

Environmental and Safety Concerns

Environmental and safety concerns associated with the production and disposal of thin film materials represent a critical challenge for the market. The manufacturing processes for certain thin films, such as those involving hazardous chemicals or high-energy requirements, can pose environmental risks, including emissions and waste management issues. Additionally, the disposal of thin film products at the end of their life cycle can contribute to environmental pollution if not managed properly. Addressing these concerns requires compliance with stringent environmental regulations and the implementation of sustainable practices throughout the product lifecycle. Companies must invest in developing eco-friendly materials, improving recycling processes, and minimizing environmental impact. While there is a growing emphasis on sustainability and green technologies, the challenge of balancing performance with environmental responsibility remains a key issue for the thin film material market. Ensuring that production and disposal practices align with environmental standards is crucial for the long-term sustainability of the market.

Key Market Trends

Rising Adoption of Flexible Electronics

The growing demand for flexible electronics is a prominent trend driving the global thin film material market. Flexible electronics, which include devices like flexible displays, wearable technology, and flexible sensors, rely heavily on thin film materials due to their lightweight and adaptable properties. These materials allow for the development of electronic devices that can be bent, rolled, or stretched, providing new design possibilities and functionalities. As consumer electronics manufacturers seek to innovate with more versatile and user-friendly products, the need for thin films that can maintain performance under various mechanical stresses becomes crucial. Advances in organic light-emitting diodes (OLEDs) and organic photovoltaics (OPVs) are significant examples of how thin film technology is being leveraged in flexible electronic applications. The trend towards flexible electronics is expected to continue, driven by consumer preferences for more dynamic and adaptable devices, as well as advancements in material science that enhance the performance and durability of thin films. This trend will likely propel the demand for thin film materials and drive market growth.

Increased Focus on Energy-Efficient Technologies

The global push towards energy efficiency is significantly influencing the thin film material market. Thin films, particularly those used in photovoltaic cells and energy-efficient coatings, play a vital role in reducing energy consumption and improving overall efficiency. In the renewable energy sector, thin film solar cells offer an attractive alternative to traditional silicon-based panels by providing lower production costs and improved performance under low-light conditions. Additionally, thin film coatings are increasingly used in energy-efficient windows and buildings to reduce heat loss and optimize energy use. Governments and industries worldwide are implementing stringent regulations and incentives to promote energy-efficient technologies, which drives the demand for advanced thin film solutions. The focus on reducing carbon footprints and enhancing energy efficiency aligns with the capabilities of thin film technologies, thereby fostering market growth and innovation.

Advancements in Thin Film Deposition Technologies

Significant advancements in thin film deposition technologies are shaping the market dynamics. Techniques such as Chemical Vapor Deposition (CVD), Physical Vapor Deposition (PVD), and Atomic Layer Deposition (ALD) have evolved, offering improved control over film thickness, composition, and uniformity. These advancements allow for the production of high-quality thin films with enhanced properties such as increased conductivity, better durability, and superior optical characteristics. The development of more efficient and scalable deposition methods is crucial for meeting the growing demand for thin films in various applications, including semiconductors, displays, and solar cells. The continuous innovation in deposition technologies enables manufacturers to address the challenges associated with producing advanced thin films and supports the expansion of their applications. As these technologies become more refined and cost-effective, they will drive further growth in the thin film material market.

Growing Integration of Thin Films in Smart Technologies

The integration of thin films into smart technologies is a key trend influencing the market. Thin films are increasingly being incorporated into smart devices, such as sensors, displays, and advanced control systems, due to their ability to provide essential functionalities in a compact form. For instance, thin film transistors (TFTs) are crucial components in smart displays, while thin film sensors are used in various applications ranging from health monitoring to environmental sensing. The proliferation of Internet of Things (IoT) devices and smart infrastructure highlights the growing need for thin film materials that offer high performance and reliability. As smart technologies advance and become more prevalent, the demand for thin film materials that can meet the performance requirements of these applications will continue to rise. This trend underscores the importance of thin films in enabling the next generation of smart and connected devices.

Increased Research and Development in Advanced Materials

There is a notable trend towards increased research and development (R&D) in advanced thin film materials. Companies and research institutions are focusing on discovering and developing new thin film materials with enhanced properties and functionalities. Innovations in material science are leading to the development of thin films with improved electrical, optical, and mechanical characteristics, which are critical for expanding their applications across various industries. For example, research into new organic and inorganic materials is yielding thin films with higher efficiency and durability, making them suitable for advanced applications in electronics, energy, and coatings. Additionally, R&D efforts are aimed at optimizing manufacturing processes to reduce costs and improve scalability. The emphasis on R&D is driving the advancement of thin film technologies, fostering innovation, and creating new opportunities in the market. As research continues to push the boundaries of what thin films can achieve, it will support the growth and evolution of the global thin film material market.

Segmental Insights

Type Insights

The Cadmium Telluride (CdTe) segment dominated the global thin film material market and is expected to maintain its leadership throughout the forecast period. CdTe thin films are widely utilized in the photovoltaic (PV) sector due to their high efficiency and cost-effectiveness in converting solar energy into electricity. The CdTe technology benefits from a favorable balance between efficiency and manufacturing costs, making it a preferred choice for large-scale solar power installations. This type of thin film offers several advantages, including lower production costs compared to other thin film technologies and a high absorption coefficient, which allows it to capture a significant amount of sunlight even with a thin layer. The established manufacturing processes and extensive industry experience with CdTe further bolster its dominance. Additionally, ongoing advancements in CdTe technology are enhancing its performance and efficiency, contributing to its sustained market leadership. Despite the strong presence of other types such as Copper Indium Gallium Selenide (CIGS) and Amorphous Silicon (a-Si), which also offer valuable properties and applications, CdTe remains the dominant segment due to its established market position and technological advantages in cost and efficiency. As the demand for renewable energy solutions continues to grow, the CdTe segment is well-positioned to leverage its benefits, ensuring its dominance in the thin film material market throughout the forecast period.

Regional Insights

Asia-Pacific emerged as the dominant region in the global thin film material market and is projected to sustain its leading position throughout the forecast period. The region's dominance can be attributed to several key factors. First, Asia-Pacific hosts major manufacturing hubs and technology centers for thin film materials, driven by significant investments in semiconductor, photovoltaic, and electronics industries. Countries such as China, Japan, and South Korea are at the forefront of thin film technology development, benefiting from robust industrial infrastructure, advanced research capabilities, and competitive manufacturing costs. Additionally, the region's rapid industrialization and expanding renewable energy initiatives contribute to high demand for thin film materials. China, in particular, is a major player in the photovoltaic sector, driving substantial demand for thin film technologies in solar energy applications. The region's favorable government policies, incentives for renewable energy projects, and substantial domestic and international market growth further bolster its position. The Asia-Pacific market also benefits from a growing consumer electronics sector, which increasingly incorporates thin film technologies in devices such as smartphones, tablets, and flexible displays. As technology advances and manufacturing processes become more efficient, the region is well-positioned to continue leading the thin film material market. The combination of strong industrial capabilities, strategic investments, and supportive policy frameworks ensures that Asia-Pacific will maintain its dominance and drive market growth in the coming years.

Recent Developments

- In May 2023, Sharp Corporation hasunveiled a significant advancement in micro-LED technology, showcasing its newultra-high-resolution display panel at the latest industry event. Thisbreakthrough promises to enhance visual clarity and color accuracy, setting anew benchmark in display technology. The development positions Sharp at theforefront of the display market, catering to the growing demand forhigh-performance, energy-efficient visual solutions across variousapplications. This innovation underscores Sharp's commitment to drivingtechnological progress in the display sector.

Key Market Players

- First Solar, Inc.

- Hanergy Thin Film Power EME B.V.

- Ascent Solar Technologies, Inc.

- SunPower Corporation

- Sharp Corporation

- Meyer Burger GmbH

- LG Display Co., Ltd.

- Kodak Alaris Inc.

- Shoei Electronic Materials, Inc.

- Applied Materials, Inc.

- Vital Materials Co., Limited

- Ferroperm Optics A/S

|

By Type |

By End-use Industry |

By Region |

|

|

|

Related Reports

FAQ'S

For a single, multi and corporate client license, the report will be available in PDF format. Sample report would be given you in excel format. For more questions please contact:

Within 24 to 48 hrs.

You can contact Sales team (sales@marketinsightsresearch.com) and they will direct you on email

You can order a report by selecting payment methods, which is bank wire or online payment through any Debit/Credit card, Razor pay or PayPal.

Discounts are available.

Hard Copy