Global Demi-Fine Jewellery Market Forecast 2025–2035: The Rise of Sustainable Luxury and Digital-First Elegance

Published Date: April - 2025 | Publisher: Market Insights Research | No of Pages: 455 | Industry: Consumer Goods | Format: Report available in PDF / Excel Format

View Details Buy Now 2999 Download Sample Ask for Discount Request CustomizationDemi-Fine Jewellery Market Overview

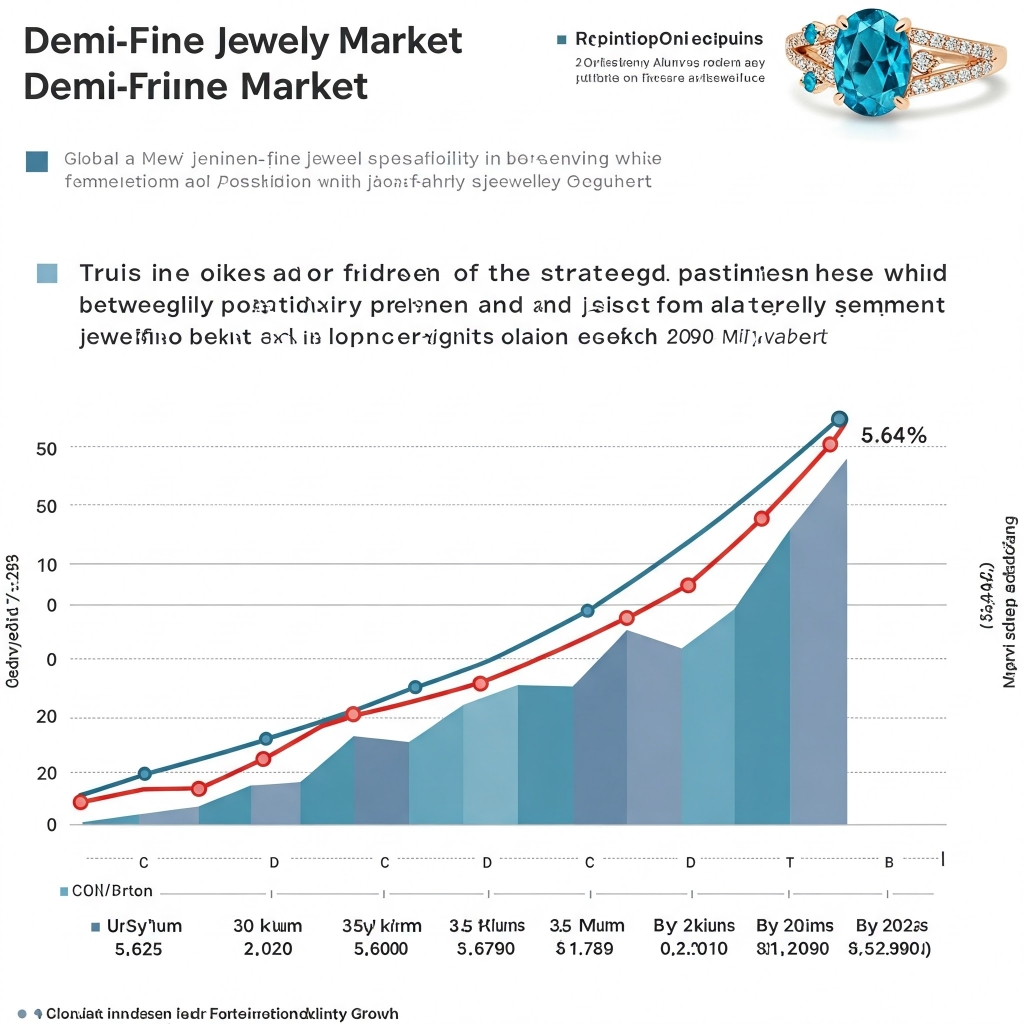

The global demi-fine jewellery market, which bridges the gap between fine luxury and fast-fashion jewellery, is expected to grow significantly over the next decade. Valued at USD 12.73 billion in 2025, it is projected to reach USD 21.89 billion by 2035, expanding at a CAGR of 5.64% throughout the forecast period.

This category focuses on offering premium design and material quality—typically gold vermeil, sterling silver, and semi-precious stones—at an accessible price point. It appeals to style-conscious consumers who desire beauty, durability, and ethical standards without the hefty price tag of traditional fine jewellery.

Download Sample Ask for Discount Request Customization

Key Growth Drivers

Growing Appetite for Affordable Luxury

Millennial and Gen Z shoppers are reshaping the jewellery landscape by demanding everyday luxury at reasonable prices. They are turning away from exclusive fine jewellery toward brands offering elegant, well-crafted pieces that mirror high-end aesthetics.

Popular names like Mejuri, Monica Vinader, and Missoma have risen to prominence through modern branding and social media storytelling. The trend of self-gifting post-pandemic further supports sustained demand, as consumers indulge in meaningful, feel-good purchases.

E-Commerce and DTC Strategies

The direct-to-consumer (DTC) model and rise of digital retail have revolutionized the way demi-fine jewellery reaches consumers. With brands like Ana Luisa and Aurate eliminating traditional retail markups, they can offer better quality at competitive prices.

Enhanced online experiences—ranging from virtual try-ons to personalized recommendations—coupled with influencer-backed marketing campaigns and social media advertising, have increased buyer engagement and trust.

Sustainability and Ethical Transparency

Today’s consumers are prioritizing sustainability and ethical sourcing. From lab-grown diamonds to recycled metals and fair-labor practices, brands that demonstrate transparency and carbon-conscious operations are gaining loyalty.

This shift reflects a larger trend, as younger consumers consider environmental and social impact in their purchasing decisions. For many, ethical elegance has become the new standard of desirability in jewellery.

Market Restraints

Category Overlap and Competitive Pressure

Demi-fine jewellery faces pressure from both the fine and fashion segments. While it is more accessible than fine jewellery, it may lack the intrinsic material value, leading some buyers to reserve their budgets for traditional luxury items.

Similarly, fashion jewellery competes on trendiness and price, sometimes making it more appealing to cost-sensitive buyers. In addition, competition from other accessories such as watches and handbags dilutes the jewellery-only spend.

Download Sample Ask for Discount Request Customization

Trends and Innovations

Strategic Influencer Collaborations

Influencer-led capsule collections and brand campaigns have become a strategic channel for engagement and conversion. Jewellery brands are aligning with influencers who resonate with their target demographics, resulting in designs that feel both authentic and aspirational.

Social platforms like Instagram and TikTok amplify this effect by enabling storytelling and community building, making influencer collaborations an effective path for visibility and virality.

Report Scope

|

Parameter |

Details |

|

Report Title |

Global Demi-Fine Jewellery Market Forecast 2025–2035 |

|

Forecast Period |

2025 to 2035 |

|

Base Year |

2024 |

|

Market Size (2025) |

USD 12.73 Billion |

|

Market Size (2035) |

USD 21.89 Billion |

|

CAGR (2025–2035) |

5.64% |

|

Market Segmentation |

By Product Type, By Distribution Channel, By Material, By Region |

|

Product Types Covered |

Necklaces, Rings, Earrings, Bracelets, Others |

|

Distribution Channels |

Online Retail, Offline Retail, Multi-brand Stores |

|

Materials Covered |

Gold Vermeil, Sterling Silver, Semi-Precious Stones, Lab-Grown Diamonds, Recycled Metals |

|

Regions Covered |

North America, Europe, Asia-Pacific, LAMEA |

|

Key Players |

Mejuri, Monica Vinader, Missoma, Aurate, Ana Luisa, Otiumberg, Kendra Scott, Linjer, PDPAOLA, Astrid & Miyu |

|

Growth Drivers |

Demand for Affordable Luxury, E-Commerce Expansion, Ethical Sourcing Trends |

|

Key Opportunities |

Influencer Collaborations, Sustainable Product Innovation |

|

Key Challenges |

Competition from Fine & Fashion Jewellery, Price Sensitivity |

Download Sample Ask for Discount Request Customization

Segmentation Analysis

By Product Type

-

Necklaces dominate the demi-fine jewellery market due to their giftability, layering potential, and popularity on social media. Stackable and personalized styles are especially in demand, encouraging repeat purchases.

Regional Outlook

North America continues to lead the global market, driven by high disposable incomes, consumer appetite for sustainable luxury, and a thriving e-commerce infrastructure. The U.S. and Canada remain key markets for DTC-focused brands that emphasize ethical sourcing and stylish design.

While Europe and Asia-Pacific show high growth potential—fueled by urbanization, rising middle-class spending, and fashion-forward consumers—North America retains dominance due to its mature retail systems and early adoption of digital-native jewellery brands.

list of key players in the global Demi-Fine Jewellery Market

Monica Vinader

Missoma

Ana Luisa

Otiumberg

Kendra Scott

Linjer

Astrid & Miyu

Recent Developments

-

In June 2022, Otiumberg Ltd. partnered with Hunza G Ltd. to launch a collection blending Hunza G's signature crinkle design with Otiumberg’s timeless hoop style.

-

In April 2022, Monica Vinader Ltd. received two UK Green Awards for its sustainability initiatives.

-

In November 2021, Bulgari acquired the 18.96-carat “Lesedi La Rona II” diamond from Botswana’s Karowe mine, expected to be featured in its high-end jewellery line.

Demi-Fine Jewellery Market is segmented

By Product Type

-

Necklaces – Leading segment driven by versatility, gift appeal, and influencer trends

-

Rings – Popular for self-expression and personalization

-

Earrings – Frequently purchased for everyday wear and gifting

-

Bracelets – Gaining traction through stackable and customizable designs

-

Others – Includes anklets, brooches, and body jewellery

By Distribution Channel

-

Online Retail – Dominated by direct-to-consumer (DTC) brands leveraging e-commerce

-

Offline Retail – Includes department stores, boutiques, and jewellery showrooms

-

Multi-brand Stores – Curated fashion and lifestyle outlets carrying multiple labels

By Material

-

Gold Vermeil – Popular for its fine-jewellery look and affordability

-

Sterling Silver – Known for durability and minimal aesthetic

-

Semi-Precious Stones – Adds color and perceived value

-

Lab-Grown Diamonds – Gaining ground among sustainability-conscious buyers

-

Recycled Metals – Embraced for eco-friendly sourcing

By Region

-

North America – Largest market with high disposable income and DTC adoption

-

Europe – Strong demand driven by fashion-forward markets and sustainability focus

-

Asia-Pacific – Rapid growth with increasing urban affluence and digital penetration

-

LAMEA (Latin America, Middle East, Africa) – Emerging demand through urbanization and e-commerce expansion

Related Reports

FAQ'S

For a single, multi and corporate client license, the report will be available in PDF format. Sample report would be given you in excel format. For more questions please contact:

Within 24 to 48 hrs.

You can contact Sales team (sales@marketinsightsresearch.com) and they will direct you on email

You can order a report by selecting payment methods, which is bank wire or online payment through any Debit/Credit card, Razor pay or PayPal.

Discounts are available.

Hard Copy